The basic purpose of life insurance is to create cash in case of sudden demise of a bread earner. Unfortunately, planning of death benefit for potential dependents is often ignored. In India, life insurance policies are sold as savings, tax sheltering schemes. As a result, the insured (bread earner) is misled.

Being Financial Advisor in Kolkata, we write Financial Plan for our clients with the objective of meeting life goals through certain processes. But the question is “If the bread earner dies untimely, how will the life goals be met?”

With death, income of bread earner ceases. So, we design the Financial Plan for our clients, which includes element of protection, planning for contingencies or emergencies, risk profiling, goal planning, retirement planning, wealth creation, cash flow planning, net worth, debt planning etc.

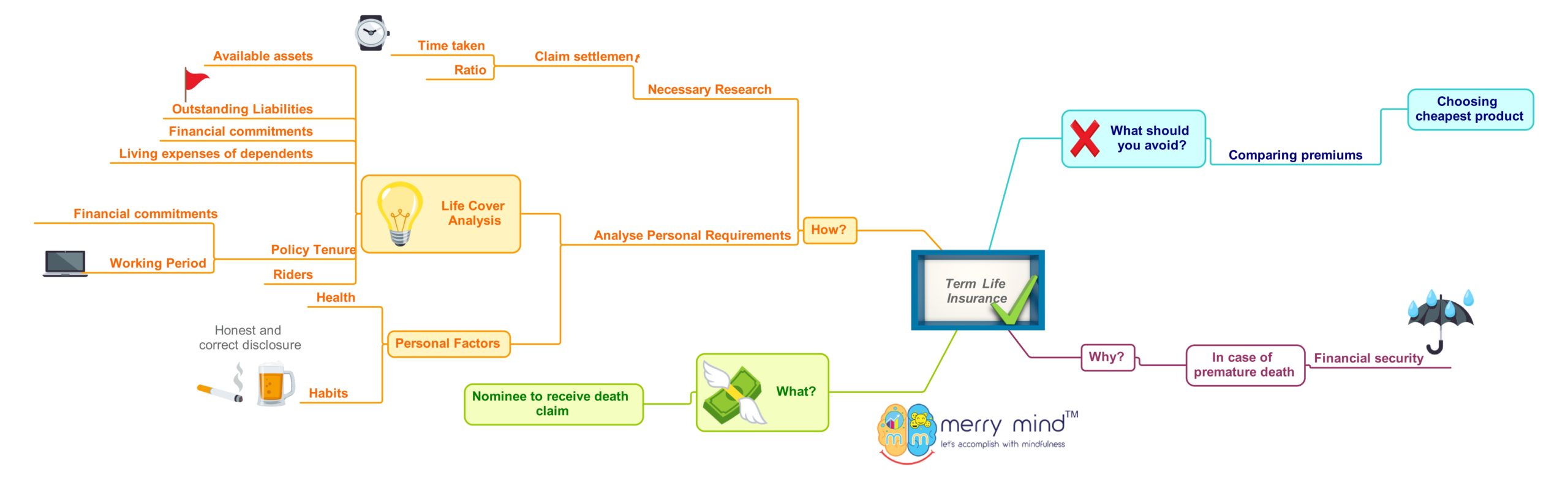

No one can ignore the importance of life insurance. A genuine Financial Advisor considers insurance (both life and non-life) as the foundation of your financial life while writing your Financial Plan. In your absence, due to untimely death, life insurance coverage replaces your income and meet your unfulfilled family commitments like:

- Repayment of outstanding liability

- Family Goals & Commitments:-

- Children’s Education & Marriage

- Meeting of daily needs of potential dependents like parents, in-laws etc

- House Purchase (First House only)

- Corpus required for following expenses:-

- Household Expenses of nearest family members like spouse and children

- Lifestyle Expenses of nearest family members like spouse and children

- Other Expenses:-

- Medical cost for breadwinner if s/he spends more than medical coverage before death

- Funeral expenses etc.

In most of the cases, people think premium of life insurance is a liability on them. They give least priority. If you think about the benefits of pure life insurance, it’ll not pinch your purse. While you think of life insurance as savings/investment, tax savings tool, it’ll pinch you definitely. The approach to consider life insurance as savings or investment or tax savings tool is fundamentally wrong. As you have other suitable options for investment and tax savings tools, you need to just diversify your investments and tax savings according to your subjective requirements. If you buy endowment insurance or ULIP, you may be looking at insurance from different perspective. It’s advisable to buy adequate term insurance and invest your surplus money in other investment baskets as per your risk profile, objective, investment time horizon, personal and macroeconomic factors.

Life is unsecured and inflation as well as taxes are unavoidable. That is the reason why term life insurance is considered by Financial Advisors to be the most suitable for creating a legacy 15-20 times or more according to Human Life Value Calculation or Capital Need Analysis so that your annual household expenses, liabilities and financial goals can be met without having to pay huge premiums compared to traditional life insurances.

What is a Term Life Insurance?

It’s basically a pure insurance (income protection plan) life cover which provides economic protection to the person for a certain period of time. Ideally, the breadwinner must have cover till s/he has earned income span or till retirement, which is suitable. In case of untimely death of the bread earner during the period of the coverage, the nominee receives the sum insured. The term insurance policy is unlike endowment plans or traditional insurance policies. A term plan doesn’t have any investment component & therefore It’s cheaper than traditional insurance plans. It’s designed with the concept of “least for the most”. It’s also called pure insurance.

The Economic Basis of Life Insurance

Throughout the world, life insurance has social and economic influences and this has been expanding remarkably. It is well recognized that the broad mission of life insurance is to protect against the total (presumably) permanent loss of human life value in monetary terms when that loss is occasioned by the economic destruction of the insured life.

The basis of life insurance is the monetary worth of human life – the factors of human life value are health, education, training and experience, creativity and attitude etc. If there is no human life value, there would be no property value as well. Human life value is the cause rather than the effect. Human life is the income producer (what human life can generate or produce). Example, if you’ve purchased a house at Rs. 90,00,000 (residential asset), the residential house is the effect and you are the cause. As you’re the cause, your life insurance value is more than the effects, if you’re insurable.

Protection of Human Life Value against Death

We know the most certain and universal truth is death, but the time of death is uncertain. Just as property is exposed to destruction by fire, earthquake, and other perils, similarly monetary worth of human life is continuously subject to destruction by loss of current earnings power through death or to serious diminution through temporary or permanently disability occasioned by sickness or accident. Life insurance contract simply involves the promise to pay a pre-determined sum by one party (the insurer) to another party (the insured or the nominee) upon the payment of stipulated consideration (the premium) and subject to specified conditions of contract. The primary purpose of life insurance is to guarantee dependents of the insured against loss of his current earning power through death.

While we are apt to construe death only in the light of physical death, the concept needs to be given an economic interpretation. The stated purpose of life insurance is to serve economically the loss of current earning-capacity when the loss is occasioned by the economic destruction of the insured life. The important point to note is that the working life of income-producing individual has ended and the particular form that it takes relatively unimportant. From an economic standpoint, the permanent loss of income earning-capacity may take any one of the three forms: (1) physical death, (2) total & permanent disability or living death, & (3) retirement.

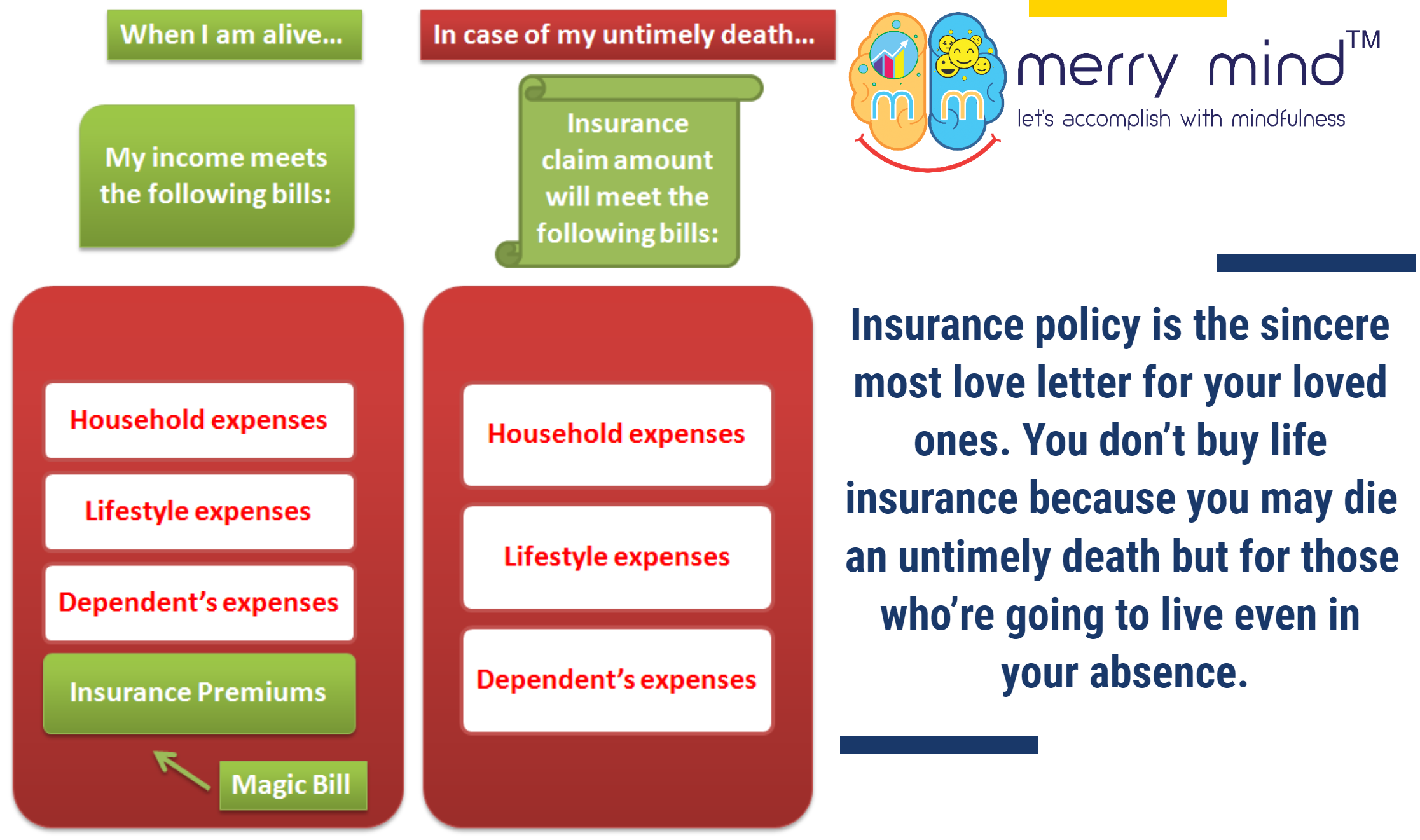

We say life insurance premium as magic bill. When you don’t have the capacity to pay your bills due to premature death or permanent & total disablement due to accident; you need not to pay the insurance premium anymore. Rather your insurance claimed amounts take care of other bills (household, lifestyle and dependent’s expenses).

Before you buy life insurance, you should know whether you are getting the right insurance product for yourself. Go through the policy wordings within the cooling-off period. Your needs are different from others, you have to understand your uniqueness. One-size-fits-all approach never works for everyone in case of personal finance.

Try to understand the basics:

- What is life insurance?

- Why do you require life insurance? and

- How much do you require?

If you do care about above concerns and you want to be insured adequately, then insure your life for its full economic value. If you are unable to figure out your required insurance amount, you may consult with a Certified Financial Planner and/or SEBI Registered Investment Advisor in Kolkata. You need a comprehensive analysis which measures financial needs and presents sound solution when you don’t have earned income due to pre-mature death or permanent & total disablement due to accident.

In this article, we have covered the need of life insurance only and there are also non-life insurances (General Insurance).

As Certified Financial Planner in Kolkata , we understand our role of assessing your personal aspects and risks, which are process oriented. Then, we incorporate risk assessment and risk protection into your detailed Financial Plan. By analyzing the individual risk areas, the extent and type of protection best suited for your financial situation and financial goals, your Financial Planner will share the recommendations.

While you propose for life insurance, never suppress any material fact. Life insurance is a contract based on mutual trust between the two parties (insured and insurer) and is primarily built on the principle of “utmost good faith” wherein both the insured and the insurer are required to disclose all the relevant information (facts) to each other honestly. If you suppress any material information, your policy becomes null and void and the nominee will not receive the claim amount.

Mind it, your health and money buy insurance for you, money by itself can’t buy your insurance.