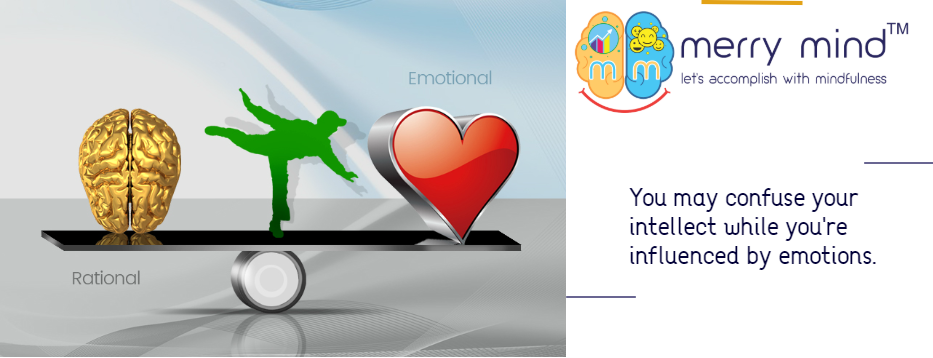

Your financial freedom is disrupted once you are driven by emotions, i.e. anxiety, happiness, sadness, fear & greed. This happens when you follow your heart without allowing your mind to apply logic. Thus, you fail to plan rationally. Relying on gut feelings, underestimating or overestimating your chances of success or failure will not let you enjoy the journey towards your financial freedom. You fail to go through certain financial planning processes and ultimately become irrational. There’s a need to go beyond numbers. When you’re emotional while making any decision, you are basically trapped. Even the smart leaders often have taken bad decisions. Most of the time emotions are to blame. Sometimes you have to control your expectations logically. This is one of the roles of a Financial Planner in your life.

Emotion is an obstacle to financial freedom

Being Certified Financial Planner in Kolkata and from our elongated experience, we have been experiencing that, “Emotional loss is temporary while financial loss is permanent.” Innocence arise from pure emotions. In spite of understanding that emotions are an obstacle to financial freedom, still, you may become emotional when you take financial decisions!

One can outweigh emotional loss but it’s very difficult to outweigh financial loss. Consider the loss of a father or a sole earning member of the family during one’s dependency period. This is an emotional loss as well as a financial loss. The distressed family can somehow outweigh emotional loss in due course. Can financial loss be outweighed easily? It’s very difficult to replace the income of a deceased breadwinner. Death of a breadwinner with unfinished commitments is a disaster to a family. You must understand the logic behind taking life insurance coverage. You end up ignoring the intensity of financial loss as a result of untimely death or disablement due to illness or accident. Your objectives while taking life insurance are usually tax savings, for future provisions & lastly risk coverage. If you consider rationally, your objective should be only to cover risk and you must go for adequate life insurance (Term Insurance Plan), personal accident & critical illness insurance policy.

Emotions may influence your Investment objectives

“Investment mistakes are investor mistakes.” – Carl Richards

According to Carl Richards, it’s about the behavior gap which is the difference between investment returns and investor returns. The difference between investment return & investor return arises where your actions are driven by emotions. Your thoughts and actions reflect your emotions. Fear and greed are temporary but the effects are permanent. Effects are either loss, gain or no loss and no gain. An emotional investor becomes irrational. An investor losses his comfort level due to temporary loss or market volatility because of fear and greed. He becomes vulnerable & burns his fingers. During the bull markets, irrational investors will be eager to invest more than the wise/rational investors. An emotional investor behaves in a manner corresponding to business/economic cycles.

The wise/rational investor is blessed with the exit option in the bull markets & they prefer to enter into bearish markets.

As Financial Advisor in Kolkata, we develop investment strategies as per investment objective, time horizon of investment, risk taking ability of investor, willingness of investor to take risk, personal factors of investor, macroeconomic conditions, etc. It is advisable not to behave as a trader when you have started investing with the mindset of building wealth in the long run.

Behavioral biases are the causes of investor behavior & emotional investing. You can offset emotional loss due to business cycle but not the financial loss. With time, you forget your emotional loss & try to come back to normal life. Financial loss is too exorbitant and you may be able to hardly offset that. Therefore, you can’t generate wealth to obtain financial freedom with irrational behavior. To attain financial freedom, you have to be rational as your investment options depend on both macroeconomic & your personal factors.

Again, we want to give emphasis on emotional decisions which may be inexact. We must consider Emotion vs. Logic. Too much of biased attachment is one of the causes of emotional decisions. Our desire/expectation is the cause and we act emotionally because of that desire/expectation. Result is disaster or disruption. Emotion is the outcome of desire and attachment. Attachment interferes our ability to think clearly or rationally. The contact and attachment of the ego stimulates desire. When you’re free from attachment, you become intelligent and behave rationally.

Why you’re so biased while you take financial decisions & don’t even enjoy financial freedom?

The following are few important references to attachment found in our society or family, which is worth considering in personal finance:

Service under compensation ground

Suppose parents depend on son’s income. If the son dies during service period and if the son is married, the daughter-in-law may be compensated by a job. After few months, the daughter-in-law may leave the in-law’s house and settle herself at her convenient place. Even she may remarry. Parents can somehow offset emotional loss but can’t offset financial loss. This is because there’s no one to replace the income in the distressed family. This is how a family becomes the slave to financial freedom. The objective of this scheme is to give an appointment on compensation ground to a dependent family member of a Government Servant who was the sole earner and is no more. Therefore, the distressed family has to select the candidate rationally regarding appointment on compassionate ground if parents are financial dependent.

Nomination

Nomination is a provision by which a person can designate any person to receive the money in the event of his death. It may be applicable to bank, mutual fund, insurance company, post office etc. After death of an investor/insured, the heirs are able to establish their claim on the investment/insurance amount. In that case selection of nominee/nominees plays a vital role. Sometimes, you may nominate someone emotionally. The nominee may not perform his/her responsibilities as desired by the deceased. Although nominee has no legal status, except life insurance policy (Amended in 2015), one should be careful.

We got a call from an insured person who asked us whether he can assign his minor daughter out of love & affection as nominee. He can assign his daughter but since she is minor, I advised him to appoint his spouse as nominee. But he didn’t accept my advice. Interestingly, he wanted to appoint his spouse as a guardian. I understood that the insured is going to take an emotional decision. Sometimes, several nominees are made in favor of wife & children. It would not be free from doubt as the main purpose of nomination will be defeated. Always mention the names of wife & children, mention the % of claim amount you want to share within the nominees in case of death. You can change the nomination but the valid assignment can’t be cancelled by the assignor even though the Notice of Assignment had not been served to Insurer.

Gift

You may like to gift something to your relatives or loved one. It may be out of love and affection. One can do it voluntarily without full valuable consideration.

If you are not sure about how your son will treat you in future, be careful about gifting your property to him. The Supreme Court has ruled that parents cannot take back land or property gifted to their children on the ground of ill-treatment by the offspring after they have received the gift.

(Source: Times of India. https://timesofindia.indiatimes.com/india/Parents-cant-take-back-property-gifted-to-kids/articleshow/2629850.cms)

Will

A ‘Will’ means the legal declaration of the intention of a testator with respect to his property, which he desires to be carried into effect after his death.

While making a Will, the testator should be rational to whom he should make a disposition of his property to take effect after his death.

Don’t forget to keep your will updated. As life changes, so do potential beneficiaries and heirs. If you fail to keep your last will and testament updated, it may not reflect your wishes given your new circumstances.

Business Succession Planning

If you are a business owner, you must have Business Succession Plan. For business owner, no one can ignore premature death, disablement due to sickness or accident & retirement.

After all, one has to decide whether succession plan is at all required or not. One may sell the business. However, many owners may prefer to continue even after their death, disablement or retirement. It’s not so easy to choose a successor rationally. For which one need Succession Plan as well. One is prudent who plans beforehand.

Purpose of this article is to make you aware about the consequences of emotional/biased and realistic /rational/analytical decisions. Therefore you have to balance logical mind Vs. Emotional heart.

To conclude, as SEBI Registered Investment Advisor in Kolkata, we can say that, knowing the difference can help investors maintain the proper perspective when making financial decisions towards financial freedom. Think about your inner purpose & objective rationally. While you need to take any financial decision, take some time and rethink when you’re calm & sunny. Minimize your assumptions. We all like to enjoy financial freedom. But, mere thinking is not enough. You will have to implement your thoughts into action mindfully with periodical reviews rationally.

Excellent article, Sir! I can relate my own story with this article. In my early earning days, I invested most of my savings as life insurance policies , but there was not a single term plan, as the insurance agent was one of my relatives and took (undue?) advantage of my emotions. He told me how that insurance company will return a huge amount (my greed) on maturity and how my policy will protect my family (my anxiety, fear of death) in my absence. However I cannot blame him as he was just a mere insurance agent, not a financial planner. Unfortunately I was ignorant and never came across an article like this. As a result , now I am struggling to reach the point of my financial freedom. Hope other will follow this article and balance their emotions and enjoy their financial freedom.

Thank you for your comments. In spite of pushed products, one needs proper solution of his/her problem.

I appreciate your valuable inputs which you shared from your experience. Great learning from experiences.

Keep on sharing your views. Sole motive of these articles is to increase awareness among all.