Many investors randomly invest without following any particular Investment Plan. Investment Plan is a part of your Financial Plan. Investment Plan emphasizes on processes. It helps you to achieve your financial goals or objectives in a systematized way.

As per your Financial Plan, you may have short term, medium term and long term goals. The fundamental law of investment is “risk and return go hand in hand.” Your economic well-being depends on your rational behavior, compact investment plan and informed decision-making ability. If you’re impulsive, you can hardly take pleasure of financial freedom. Your impetuous acts are your biggest antagonist.

“In investing, what is comfortable is rarely profitable.” – Robert Arnott

While we construct Investment Plan (based on your Financial Plan) we consider the following subjective inputs

- Your personal (health & family structure) & financial status,

- Your Goal i.e. may be retirement, house purchase, children’s provision like higher education, marriage, start-up, house purchase, car purchase, international vacation and other high-end goals,

- Current age,

- Numbers of years for each goal,

- Rate of yearly inflation,

- Expected rate of return based of risk profile (need asset allocation),

- Your income growth,

- In case of retirement, your longevity,

- In case of retirement, your current expenses,

- In case of retirement, assumption of income tax bracket,

- Your existing asset utilization & employment benefits,

- Investment strategy,

- Strategy implementation,

- Investment evaluation,

- Investment monitoring & re-balancing as market scenario,

- Deficit,

- Surplus for investment,

- Your priority of investment, etc.

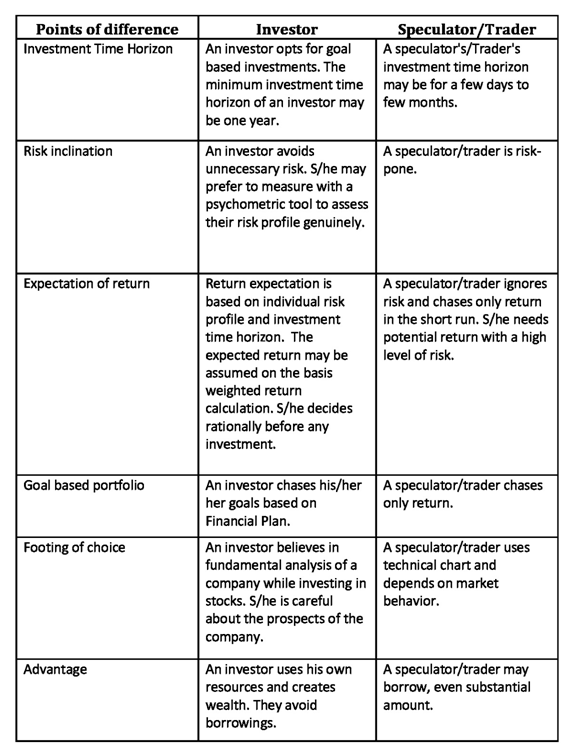

Distinguish an investor from a speculator

An investor sacrifices current consumption for wealth creation. Numerous investment instruments are available today. The objective is to protect your purchasing power. We stumble across so many investors who invest randomly in Mutual Funds, Stocks, Bank FDs, Life Insurance, PPF, Post office and Real Estate or other instruments. Neither do they have purposes, nor do they get any quality advice or suitable solution. It’s because of their herd mentality and limited knowledge. Mostly they focus on rate of return. They fail to assess their risk tolerance capacity and product suitability. Rate of return is one of the many factors – this is not the sole factor! Investor’s illogical expectations impede wealth accumulation and wealth creation in the desired term.

If the risk profile mismatches with your investments, you may lose your principal. Thus, you’ll be unable to reach your financial goals. Traders hold a stock for short term. An investor has to distinguish himself/ herself from a speculator while s/he invests in stocks or mutual funds. We think traders hardly need any Investment Plan. Trading is pure speculation and they’ve nothing to do with Investment Plan.

There may be many subjective concerns. Being a Certified Financial Planner in Kolkata, we are surprised while an investor behaves like a speculator. Speculators are traders; they make profit/loss from trading. On the other hand, an investor creates wealth to achieve goal/s within a specific period.

Let’s discuss about the points of difference Investor Vs Speculator/Trader:

“The individual investor should act consistently as an investor and not as a speculator.” – Ben Graham

In which category do you belong? Are you an investor or a trader/speculator?

Ask yourself if you’re an investor

- Why are you investing?

- What are your investment goals?

- What is important to you, i.e. return on investment or achievement of goal/s?

- What are your investment time horizons of different goal categories?

- What is the expected inflation rate?

- What is your risk tolerance level?

- How much risk taking capacity you have?

- What are your existing investment assets those are to be mapped with your goals?

- Have you ever quantified the deficit amount?

- What is your surplus income for investments?

- Do you have investment priority as per goal?

- Do you have adequate contingency fund in place?

- Do you have adequate insurance in place? and

- What is your income growth?

What is risk in investment?

Basic concept of risk means the chance of a loss. There may be a deviation from expected return.

There are two main concerns while we analyze risk

- Where is the risk?

- How serious is the risk?

Historically, for a period of short-term investment time horizon even for few years, lower-risk investments provide better return than higher-risk investments. For long-term investments higher-risk investments provide better return than lower-risk.

Types of Risk

- Market Risk;

- Re-investment Risk;

- Interest Rate Risk;

- Purchasing Power Risk;

- Liquidity Risk;

- Political Risk;

- Exchange Risk;

- Credit/Default Risk &

- Financial Risk.

Investment Risk Illustration

No Risk: Investment in a Government of India 7.75% Savings (Taxable) Bond, 2018 has any risk. Since the bond payments are guaranteed by the Govt. of India and there is no variance.

Risk: Investment in a stock has risk. The dividends are not guaranteed by the issuer and there is a variance of return.

Measuring & classification of risk is an important part of Investment Plan

Pure Risk means there is a possibility of loss or no loss. There is no chance of gain in pure risk. Example: What we can insure is pure risk. It can indemnify the financial losses and no one can make profit. Therefore, pure risk is insurable.

Speculative Risk means there is a possibility of gain or loss. Investments by nature carry speculative risk. Speculative risks are taken by choice and consciously taken. Speculative risks are unlike pure risks. E.g. purchases of stock shares involve speculative risk.

Investment Risk or Total Risk = Systematic Risk + Non systematic Risk.

Systematic Risk is undiversifiable risk. This risk is unpredictable and impossible to avoid. Through asset allocation one can reduce the risk and maximize return. Systematic risk is market risk.

Unsystematic Risk is diversifiable risk and is also known as specific risk. Unsystematic risk is unique like labor strike, management problem and bad entrepreneurship etc. Company or firm has specific risk is non- systematic risk.

Standard deviation considers both systematic & unsystematic risk and measures the investment’s total risk. There are other three measures like Alpha, Beta, and Sharpe Ratio.

Mutual Fund investments are subject to market risk and stocks investments are subject to investment risk or total risk.

Relationship between risk & return

The important caveat is that there is a positive correlation between risk & return. Investors need to manage their portfolio or wealth effectively so that they can steadily achieve their financial goals instead of chasing return. Return is one of the factors of investment plan. But I have noticed that many investors visit with limited apprehension of Return and Risk. They behave irrationally. The returns they can expect depend on the asset class, investment time horizon and risk profile. In all investments there are risks. Low levels of risk are associated with low level of return and high levels of risk are associated with high levels of return. An investor who is willing to get high return should also be willing to accept losses.

An investor needs to apprehend his individual risk tolerance capacity when constructing his portfolio. Factors of risk tolerance depends on the investment time horizon, objective, priority and amount. An investment adviser is neither a magician nor God.

The relationship between risk and return is one of the fundamental concepts of investment plan. While we share the answers to the risk tolerance questionnaire with our clients to assess their risk tolerance ability, many times we notice they behave irrationally. This means that they expect a return which is double the fixed deposit but they’ll feel uncomfortable while their investments go down by even 10%! What is important while you chase return is your risk profile and risk tolerance ability.

What is rate of return (ROR)?

In finance, rate of return (ROR) is the gain or loss on an investment over a specified period of time, expressed as a percentage of invested money.

The components of Return

The components of return of an investment mean current return and capital return. Current return means periodical cash inflow, i.e. dividend income, interest income etc. Capital return means return of principal amount.

Why investors fail…

Behavioral interference to wealth creation through Investment Plan!

There are causes & consequences of behavioral interference during wealth creation. The equity market is inefficient. An asset’s market price doesn’t always reflect its true value. Many investors especially in the short run don’t make rational decision to maximize profit by minimizing risk.

It is not uncommon that many investors become impulsive and make irrational financial decisions. As SEBI Registered Investment Advisor in Kolkata, we go for asset allocation while developing investment strategies. Asset allocation depends on risk profile and investment time horizon. In spite of asset allocation based on clients’ profile, they can’t absorb temporary deviations. An Investment Adviser never takes investor’s irrational behavior lightly. When equity performs well, most of the investors become impulsive buyers and dictates his/her adviser to buy more. Although the planner prefers asset allocation. It has been observed that Indian investors are vulnerable and fail to achieve their goals due to following predicaments:

- Buying expensive stock & selling at low price,

- Buying when others are buying & selling when other are selling,

- Not having Financial Plan,

- Overwhelmed by media hypes and believe what they read or hear,

- Investors behave like speculator as they fail to understand the objectives,

- Investors are not aware of their risk taking ability,

- Due to lack of financial and numerical illiteracy,

- Investors behave irrationally when they become victims of greed and fear,

- Inconsistent behavior,

- Chasing return instead of goals,

- Investors try to time the market instead of giving time to market,

- Lack of required knowledge and experience as they don’t hire professional Financial Planner, etc.

Don’t believe on random online media posts, brokers or relationship managers who intend to sell you financial products. Please note that ideas which apparently look like free of cost advice are detrimental for wealth building. Your unrealistic optimism of financial success is never achievable. It doesn’t happen in real life. Thus, you have to understand economic cycle. Recall subprime crisis that took place at the end of 2007. A mortgage crisis caused panic and financial crisis all over the world. The financial market was volatile. It lasted for several years. Irrational investors lost their hard earned money due to fear. Therefore solid Financial Plan is required to be on track.

Benefits of Investment Plan

Investment Plan is needed to attain financial goals smoothly. Due to complexity of financial products, economic recession, income tax and rampant inflation you need Investment Plan before you start investments. Various types of risks are associated in any investment product and you may either be confused or overwhelmed at the time of investment decisions. Thus you can’t arrive at right strategy. There is also a chance of costly investment mistakes.

Do-it-yourself (DIY) investing has their pitfalls if you have lack of financial acumen. It is true that you can save money on fees. You can take investment decisions of your own. However, a professional advice is emotionless and unbiased. Due to limitation in DIY investing, one can hardly achieve financial goals.

A financial planner’s professional guidance is required while the investor has no experience or idea about suitable investment products or insurance solutions. The most commonly used instruments to become wealthy are cash, equity, bonds and real asset or property. They have different characteristics. Thus investment plan recommends you suitable financial products as per your profile.

Can you achieve your financial goals without plan in modern days? A sturdy Investment Plan helps you to attain the financial goals in time.

Selling of Investment Products

Investment product sellers never consider the product suitability while they sell. They sell financial products to earn commission and achieve their sales target. They intend to sell product that gives them maximum commission.

Following Investment Plan

Vs

Buying of Investment Products through salesmen

Investment Plan and Financial Plan are not same. Financial Plan consists of goals, net worth, cash flow, contingency planning, insurance planning, tax & estate planning and debt planning, etc. There may be Investment Plan in Financial Plan. But, it may not be extensive. Investment Plan is the process of resolving how to map the current investment assets and recommend future investments with proper asset allocation based on client’s profile.

In general, no financial product is associated with the unique needs of a client. It’s the Financial Planner who begets investment plan keeping in mind client’s uniqueness. Investors are influenced by the name of products/funds.In practice, these name are not associated with the client’s unique needs. For example, “XYZ Retirement Solution Fund” has a general investment objective and it’s lacking of unique needs. Therefore, names are non-connotative. Any relationship based on commissions or other form of transition fees is subject to a deep-rooted conflict of interest. Therefore, Investment Plan and selling of investment products are antipodal.

To conclude, before you start investment you must have an Investment Plan. It defines your goals for your future direction as plan always has a purpose and be rational while investing to reach your aspirations.