Once we were asked by one of our doctor clients that his friend gets free of cost investment advice & financial plan from a distributor. We asked our client, “Being a surgeon, do you operate your patients without fee?” If you do so, how will you be compensated?” We briefed him the concept of Direct Plan vs. Regular Plan in Mutual Funds & insights into the holistic financial planning processes. He then smiled and said, “Now, I understand.”

While you invest in Mutual Funds, you have two options. You may prefer either Regular Plan or Direct Plan of Mutual Fund schemes. There is no other characteristic difference between Regular Plan & Direct Plan, except expense ratio. You need to understand the delineation of Regular Plan vs Direct Plan in Mutual Fund before you start investing. You may hire a professional for proper unbiased guidance.

Securities and Exchange Board of India (SEBI) came out with many amendments in Mutual Fund industry in September 2012. They launched Direct Plans of Mutual Fund schemes. Investors can invest directly with the Asset Management Co. (AMC) in Direct Mutual Funds without paying any commission to distributors. This is what is called “Do It Yourself” i.e. “DIY”. Direct Plan option is given to an investor to purchase/subscribe units of a scheme directly with the fund and not through a distributor w.e.f 1st Jan 2013. Alternatively, an investor can invest in Direct Plans of Mutual Fund schemes after seeking unbiased advisory services against a fee from a SEBI Registered Investment Adviser.

What is expense ratio in a Mutual Fund scheme?

It’s per unit cost of management of mutual fund charged by the Asset Management Company. These costs include expenses for fund management, administration, advertising and paying sales commissions to mutual fund distributors (operating expenses). The returns of all Mutual Fund Schemes are calculated on the Net Asset Value. The expenses are deducted from the investor’s fund on daily basis from asset value. The asset value arrived thereafter is Net Asset Value.

Duties and Responsibilities of a Mutual Fund Distributor

A distributor is an individual or an entity who facilitates an investor to buy and sell units of Mutual Fund schemes. A distributor earns trail commissions for boarding investors into the Mutual Fund investments.

A Mutual Fund Distributor has the right to make an investor aware of various schemes of Mutual Funds and their features. Mutual Fund Distributor cannot advice.

A distributor helps an investor to carry out transactions like buying, switching and redemption of their investments. Distributors/Agents are not legally entitled to give investment advice.

Regular Plan vs Direct Plan in Mutual Funds

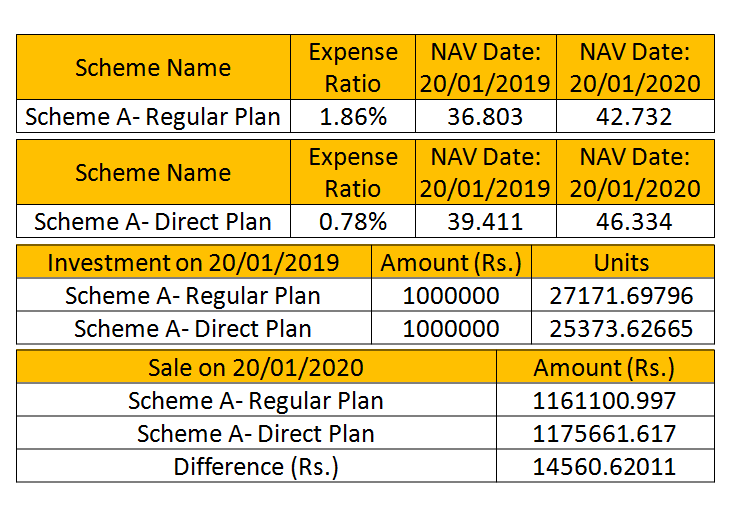

There is a long argument and controversy regarding Regular Plan vs Direct Plan. The expense ratio of Direct Plans is lower than Regular Plan. Therefore, the Net Asset Value of Direct Plan is higher than Regular Plan as there are no distribution expenses in a Direct Plan. Thus, it is commission-free. There would be no distribution and trail fees payable by investor. As the expense ratio is low, the returns (in % terms) are also higher than Regular Plan.

Who pays commission to distributor/ broker/ agent?

Asset Management Companies pay the brokerage/commission to distributor/ broker. An investor pays the commissions indirectly. The commission comes out of investor’s investment. The Net Asset Value (NAV) for a Mutual Fund scheme is calculated after all expenses/costs.

A trail commission depends on the value of the investment for each year if the investor’s money remains invested with the fund of the AMC. Apart from trail commission brokers may get upfront commission from the fresh/new investments.

Commission is a hidden/concealed cost that investors bear. Neither investors write a separate cheque nor investors get any invoice for the hidden cost. The brokers or the distributors are compensated by investors indirectly. I have given an illustration below in this article for your better understanding.

After evaluating Regular Plan vs Direct Plan, even when you hire an Investment Adviser for a fee and invest in Direct Plan of Mutual Fund schemes, you’ll be better off in the long run.

Duties, responsibilities & scope of work of a SEBI Registered Investment Adviser (SEBI RIA)

There is a difference between a Distributor and an Adviser. SEBI Registered Investment Advisers have license from the regulator to practice as an Investment Adviser. Advisers are like lawyers, doctors and architects, etc in the society. Those who need investment advice or financial plan can always contact a SEBI Registered Investment Adviser. Investors get unbiased advice/solution from SEBI Registered Investment Advisers . A SEBI Registered Investment Adviser is never driven by any sorts of commission oriented products as he will work in fiduciary capacity against a fee.

Financial Plan helps an investor to identify the goal amounts and time horizons for each goal before s/he invests in any financial instrument.

While providing investment advice, as SEBI Registered Investment Adviser, we consider the following:

- Self-discovery discussions

- Analysing objective of investment;

- Understanding of qualitative & quantitative inputs;

- Evaluating cash flow;

- Budgeting;

- Opportunity costs;

- Investment prioritization;

- Defining time horizons of investments;

- Risk tolerance & risk taking capacity of client (Risk Profiling);

- Financial Plan & periodical review of financial plan;

- Analysis of surplus for investment;

- Debt planning & repayment of debt;

- Tax planning;

- Asset allocation as per risk profile & investment time horizon;

- Goal based portfolio designing & sharing progress reports;

- Management of investors’ behavior & expectation; &

- Work with due diligence & focus conflict-free advice etc.

You may engage a SEBI Registered Investment Adviser if you’re too busy and/or have limited knowledge and information to manage your personal finance. SEBI Registered Investment Adviser can give unbiased solutions with due diligence. His/her scope of work is not to distribute of mutual fund products. He can professionally guide you across various financial instruments. He’ll make a financial plan & recommend solutions as per your product suitability. Advice given on assets are free from commissions. The scope of work of a SEBI Registered Investment Adviser is much wider than a distributor.

SEBI’s intention is to differentiate distribution of products from advice on products

Distributors can’t advise his customers and they are not allowed to give any investment advice. A distributor can’t accept any advisory fee as he gets commission by selling mutual fund products. You bear the commissions indirectly. On the other hand, a SEBI Registered Investment Adviser is not allowed to earn commission form a product manufacturer as he’s compensated by fee directly borne by his you. You may view SEBI Registered Investment Adviser as doctors and Mutual Fund Distributors/ Insurance Agents as medicine shops.

Nothing is free of cost whether an investor buys from a distributor or engages a SEBI Registered Investment Adviser. Now the question is “how much cost”, unless an investor goes for “DIY” (Do It Yourself).

Cost analysis in comparing Regular Plan vs Direct Plan

After evaluating Regular Plan vs Direct Plan, you have the following options

- You may invest through a Distributor or Salesperson or

- You may opt for “DIY” or

- Hire a SEBI Registered Investment Adviser.

How you can offset through Direct Plan?

In Regular Plan, you don’t pay directly, but expenses are adjusted from the NAV. The NAV which you see daily is calculated after deducting these expenses. As we mentioned earlier, suppose in Regular Plan an investor bears Rs. 1.86 as expenses and in Direct Plan he bears Rs. 0.78, he can save Rs. 1.08. It varies from fund to fund. A SEBI Registered Investment Adviser always recommends you Direct Plans against a fee.

Investment advisory fee should not be compared with commissions

As Financial Planners, we work holistically with our clients. We hand-hold our clients throughout their journey towards financial wellness. Along with the technical aspects, we focus on personal aspects of the clients. This helps the client as well as us to derive suitable financial plans for them. The fee you will pay your Adviser will ultimately to get peace of mind because you would want to be on trusted hands.

DIY (Investing in Direct Plan on your own)

If you’re well informed and have investment acumen then go for “Do It Yourself” (DIY). If you’ve time and research about various investment avenues, you may invest by your own in Direct Plans of Mutual Funds and other financial instruments rather than buying them through a Distributor or Salesperson. Although there is a long controversy in Regular Plan vs Direct Plan, you have to understand your limitations and opportunities. Therefore, if you have limitations (lack of knowledge of asset allocation, emotional behavior, risk profile, research, time constraint etc.), you can hire a Certified Financial Planner. You may need ongoing monitoring to ensure that investments are performing as per your needs which may change with time. You can offset your limitations by hiring a SEBI Registered Investment Adviser. Of course an Adviser may be reluctant to work with you if he’s not compensated properly.

If you need professional support, then whom to choose?

The role and scope of work of SEBI Registered Investment Adviser is extensive & research oriented. Engaging a SEBI Registered Investment Adviser for a fee and following a financial plan instead of investing through a distributor is a trade-off you’re willing to make to arrive at sound financial situation.

Ultimately, you need financial freedom. Hence, it’s better not to follow others as your requirements and objectives are different.

“You may explore, you may evaluate but you can’t execute if you are not willing to take action. Decide to take off now!”

― Israelmore Ayivor, The Great Hand Book of Quotes

You can see the scope of work of a distributor and uniqueness of a SEBI Registered Investment Adviser. Accordingly, you can engage a service provider as per your requirements. Otherwise, you may go for “DIY.”