For those who have just hung up their boots after decades of service, retirement is supposed to be a reward. It’s a time for leisure, family, and personal pursuits. Yet, for many, this new chapter is fraught with a set of unique and acute financial anxieties. Retirement planning in India is crossing the bridge from earning to enjoying – From Scarcity to Stewardship! The shift from a steady monthly income to drawing from a finite pool of funds is more than just a mathematical change; it’s a profound psychological upheaval.

For most Indians, retirement is imagined as a golden period—a time to relax, pursue hobbies, and spend meaningful moments with family. But in reality, retirement often brings with it a silent battle: financial insecurity. According to census data, India already has more than 140 million senior citizens, a number that is expected to double by 2050. Yet, despite this growing population, very few retirees enjoy true financial independence.

The challenge lies in the unspoken burdens that many seniors quietly endure. From inadequate pensions to skyrocketing healthcare expenses, the financial struggles of retirees in India often remain hidden until they become overwhelming. This article takes a deep dive into the five major financial burdens most Indian retirees don’t talk about—and offers some pathways to ease them. Effective retirement planning in India can help reduce these challenges, but awareness is the initial factor to be focused on.

1. The Psychological Shock: From Earning to Utilizing

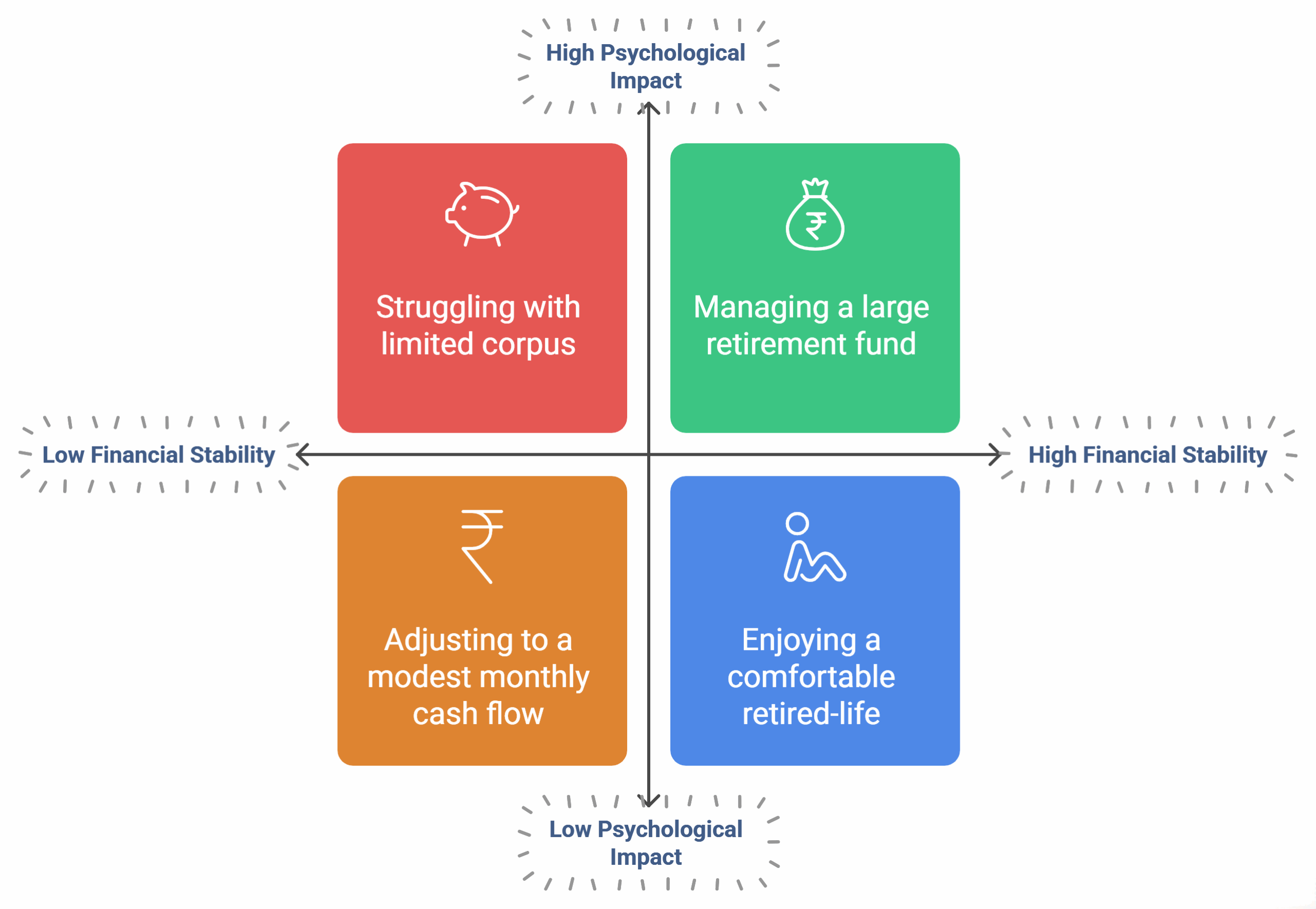

In the realm of retirement planning in India, a retiree’s sense of security was built on accumulation. For decades, every month brought new salary credits, reinforcing a feeling of growth and possibility. Suddenly, that rhythm reverses—withdrawals replace deposits, and the balance begins to recede.

- Anxiety of a Shrinking Corpus: Every withdrawal feels like chipping away at a hard-earned safety net, prompting overly frugal choices that rob simple pleasures.

- Loss of Financial Identity: Without a regular paycheck, retirees often wrestle with diminished self-esteem and a sense of lost purpose.

Recognizing these emotional tides is essential for any holistic approach to retirement planning in India.

2. The Tyranny of Inflation: Your Money Buys Less Every Day

For retirees navigating retirement planning in India, inflation is a silent eroder of stability. While employed individuals count on periodic pay hikes to offset rising costs, a fixed retirement income must stretch further year after year.

- Medical Inflation: Healthcare expenses in India have surged by 10–12% annually, far outpacing general inflation and threatening to deplete the core corpus.

- Lifestyle Erosion: Everyday costs—from groceries to travel—steadily climb, forcing unwanted compromises in quality of life.

Effective retirement planning in India must incorporate realistic inflation buffers and regular portfolio reviews.

3. The Low-Interest Rate Dilemma: The Death of “Safe” Income while doing retirement planning in India

Traditional retirement planning in India often leaned on Fixed Deposits as a low-risk income source. Low interest rates have upended this strategy, slicing the monthly yield retirees once counted on.

- Plummeting Income: What once delivered ₹50,000 per month from a ₹1 crore FD now yields far less, creating an involuntary pay cut.

- Safe No More: Maintaining purchasing power requires a judicious balance of risk and innovation, challenging retirees accustomed to stability.

As a SEBI Registered Investment Adviser in Kolkata, I am of the view that redesigning income streams is a cornerstone of modern retirement planning in India.

4. The Prime Target: Mis-selling and Financial Predators

With a visible lump-sum corpus from their retirement benefits, seniors are a prime target for financial mis-selling. This is what I could make out as I closely work with retirees as their Financial Advisor in Kolkata.

- Exploiting Trust: Relationship managers or local agents often pitch “better-than-FD” schemes with guaranteed returns.

- The ULIP & Endowment Trap: High-cost, low-liquidity plans promise tax benefits but frequently underdeliver and penalize early exits.

A robust retirement planning in India framework includes safeguards such as independent second opinions to thwart mis-selling.

5. The Burden of Complexity and Cognitive Decline

Retirement planning in India is not a one-time task; it evolves with changing laws, tax rules, and personal priorities. This constant management can overwhelm, especially when mental sharpness begins to wane.

- Management Overload: Juggling with multiple schemes, withdrawals, rent, taxes, portfolio rebalancing, and paperwork transforms retirement into a full-time job.

- Declining Financial Acuity: Complex documentation and new product pitches become harder to evaluate, increasing the risk of costly inertia or mistakes.

Streamlining accounts, automating key processes, and securing trusted support are vital within any retirement planning in India strategy.

Retirement planning in India can be reframed as a journey of purpose and freedom rather than fear and loss. As a Certified Financial Planner in Kolkata, I am of the belief that integrating these insights lay the groundwork for:

- Dynamic withdrawal plans that adjust for inflation and longevity

- Diversified income buckets combining stable and growth assets

- Digital tools and checklists for account monitoring and tax compliance

- A vetted network of advisors or family champions to review offers

- Mindset practices that shift focus from depletion to deliberate enjoyment

Each of these strategies can transform retirement planning in India from a source of anxiety into a chapter of empowered, purposeful living.

retirement planning in india should be dynamic

These pain points create a web of financial fragility. They illustrate that retirement is not a simple matter of saving money. It is a complex, dynamic phase of life where the risks are magnified and the margin for error is virtually zero. As a Fee Only Financial Planner in Kolkata, I strongly believe that addressing these deep-seated fears requires more than just investments; it requires a comprehensive, empathetic, and strategic plan.

Because true peace of mind after retirement comes not just from rest, but from financial security.