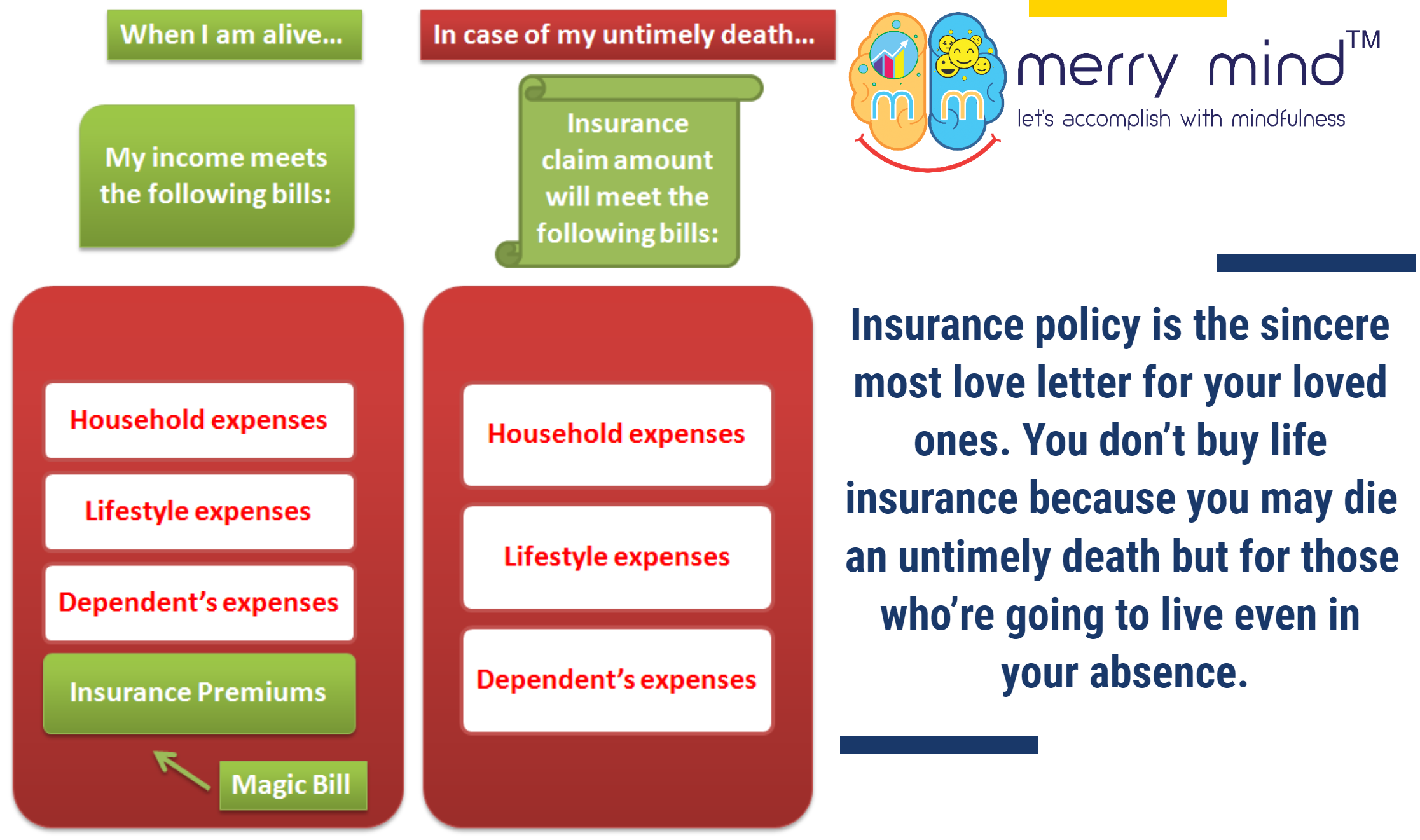

Our death is certain, but the time is uncertain. With death of bread earner, family’s income ceases but family expense doesn’t. The chief purpose of taking life insurance is to ensure family’s financial security in case of bread earner’s untimely death. Term Life Insurance fits well at every life stage. It may be considered as the least cost insurance policy.

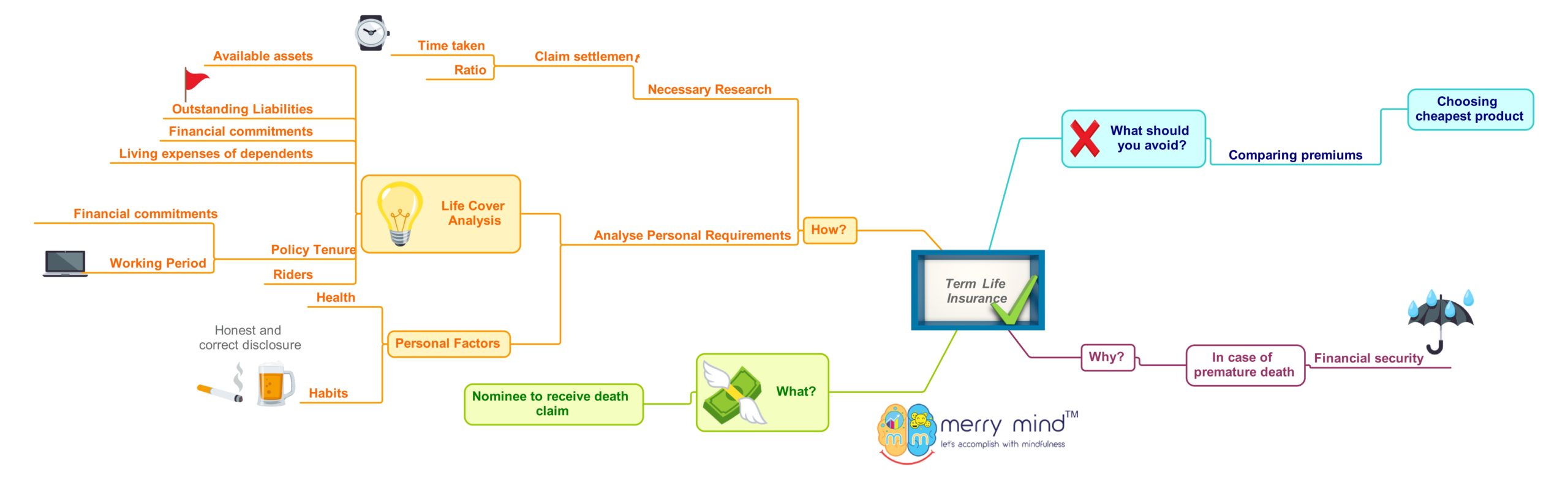

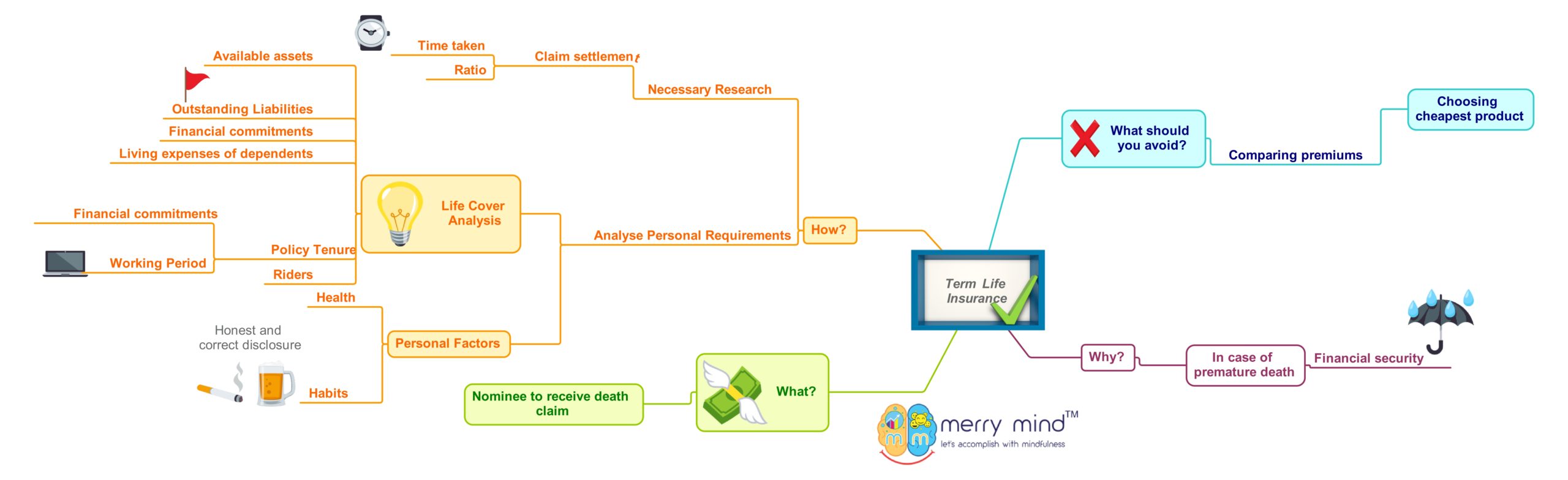

Common misapprehension in choosing Term Life Insurance policy

Information is available online in abundance. Any prospective buyer starts comparing the premium quoted by various insurance companies. Thereafter, they incline towards choosing the Term Life Insurance policy having the cheapest premium. However, this may not be the right approach of choosing a term life insurance policy.

Factors to be considered while choosing Term Life Insurance policy

Firstly, you need to thoroughly analyze personal requirements. Life cover analysis is crucial. In your absence, due to untimely death, life insurance coverage will replace your income. It is expected to meet your unfulfilled family commitments. You need to see the number of financial dependents in your family. This would vary as per your different life stages. Therefore, the life insurance cover amount needs to be reviewed at regular intervals and because of any major change in life.

You need to ensure that your family members are not stressed in order to repay existing loans (if any). You’ll certainly not want your children to compromise on their career due to lack of money in your absence. Provision for household, lifestyle and other necessary expenses of nearest family members like spouse and children (till dependency period) should be accounted for. Again, meeting of daily needs of potential dependents like spouse, parents, in-laws etc. are to be strictly considered during insurance needs analysis. Arrangements for few other expenses like meeting medical cost for breadwinner if he/she spends more than medical coverage before death, funeral expenses etc. are to be kept in mind as well while calculating insurance needs.

Often, people are in doubt while deciding the ideal tenure of his/her Term Life Insurance policy. As Financial Advisor in Kolkata, we generally recommend clients to take the cover till the age you are expecting to work and/or till the year you have financial commitments to fulfill.

Your personal factors play a significant part in analyzing insurance needs and premiums payable. Some of these factors are your age, income, profession you are in, health history, habits, etc. Having pre-existing diseases or bad habits of smoking and/or drinking not only increases the risk to your life, but also increases the premium amount for the insurance cover. You must honestly and correctly disclose all facts to insurance company while taking policy. It is to avoid rejection of insurance claims. Your loved ones would suffer and would not receive the desired financial support in hour of need if there’s misrepresentation or non-disclosure of true facts on your part.

Riders

Mostly, people waver around while buying a Term Life Insurance policy. It is because of the few extra features called the insurance riders. They come as an offer along with the base cover of a Term Plan. These benefits are optional. Usually, riders bear a cost in addition to the basic Term Plan premium.

Few of the riders are as follows:

Accidental Death Benefit Rider

Basic Term Plan covers accidental death. This rider offers additional sum assured if the death occurs due to an accident.

Example: An individual buys a basic Term Life Insurance policy of Rs. 2 Crores with an accident rider of Rs. 25 Lakhs. In case of death by accident, the nominee will get the extra pay out against accidental death of Rs. 25 Lakhs along with basic death benefit of Rs. 2 Crores.

Critical illness

This rider provides a lump sum amount if the policy holder is diagnosed with a life-threatening illness. The list of life-threatening illnesses is pre-specified in the insurance policy. The list of illnesses varies from one insurance company to another.

Accelerated Death Benefit Rider

If you are suffering from terminal illness, your family will be bearing huge medical expenses for your treatment. With this rider, you will get partial advance amount of your sum assured when you are critically ill. The remaining amount is paid to the family/nominee after your demise.

Waiver of premium

This rider is helpful in case a policy holder becomes permanently disabled due to an accident. The insurance company will waive off the future premiums while his/her policy will still be in-force.

Permanent disability

This rider also covers permanent disability. The insurance company will pay the policy holder a percentage of sum assured or a flat lump sum amount as specified in the policy.

Riders can help you to customize the coverage. They must be opted for after considering personal needs. It is absolutely important to read the terms and conditions carefully in the policy document within the free-look period.

Necessary research about insurance companies

One indicator people look at while evaluating Term Life Insurance Plans is company’s claim settlement ratio. Although it’s a broad indicator, it’s not the ultimate. This ratio indicates how much death claims a life insurer has settled in any financial year. It is calculated as the total number of claims received against the total number of claims settled. It is a historical data. With changes in underwriting guidelines, future claim settlement ratio may change. Again, claims received by the insurance company include claims against all kinds of products. It can be maturity claims and death claims.

One of the major concerns for you as a customer would be how fast a life insurance company would settle the claim. Every company reveals data on claims settled. Time taken may be varying from 1 month, 3 months, 6 months or even a year and above. You may check how many claims are pending at the end of the year.

You may visit https://www.irdai.gov.in/ for more clarification.

As Certified Financial Planner in Kolkata, we understand our role of assessing your personal aspects and risks, which are process oriented. Then, we incorporate risk assessment and risk protection into your detailed Financial Plan. By analyzing the individual risk areas, the extent and type of protection best suited for your financial situation and financial goals, your Financial Planner will share the recommendations.

In most of the cases, people think premium of life insurance is a liability on them. They give least priority. If you think about the benefits of pure life insurance, it’ll not pinch your purse. While you think of life insurance as savings/investment, tax savings tool, it’ll pinch you definitely. As SEBI Registered Investment Advisor in Kolkata, we believe that the approach to consider life insurance as savings or investment or tax savings tool is fundamentally wrong. As you have other suitable options for investment and tax savings tools, you need to just diversify your investments and tax savings according to your subjective requirements. If you buy endowment insurance or ULIP, you may be looking at insurance from different perspective. It’s advisable to buy adequate term insurance and invest your surplus money in other investment baskets as per your risk profile, objective, investment time horizon, personal and macroeconomic factors.