Systematic Withdrawal Plan (SWP) is a facility offered by Mutual Funds which allows the investors to specify withdrawal amount, withdrawal frequency and the number of withdrawals subject to availability of money in the invested scheme. For example, if an investor has invested Rs. 50,000 in a scheme and procured 500 units, he/she can set up a Systematic Withdrawal Plan to withdraw Rs. 5,000 or 50 units every quarter/month/week on a specific date for 10 quarters/months/weeks. The valuation of the scheme is subject to market movements. Systematic Withdrawal Plan is basically the opposite of Systematic Investment Plan (SIP).

Use of Systematic Withdrawal Plan

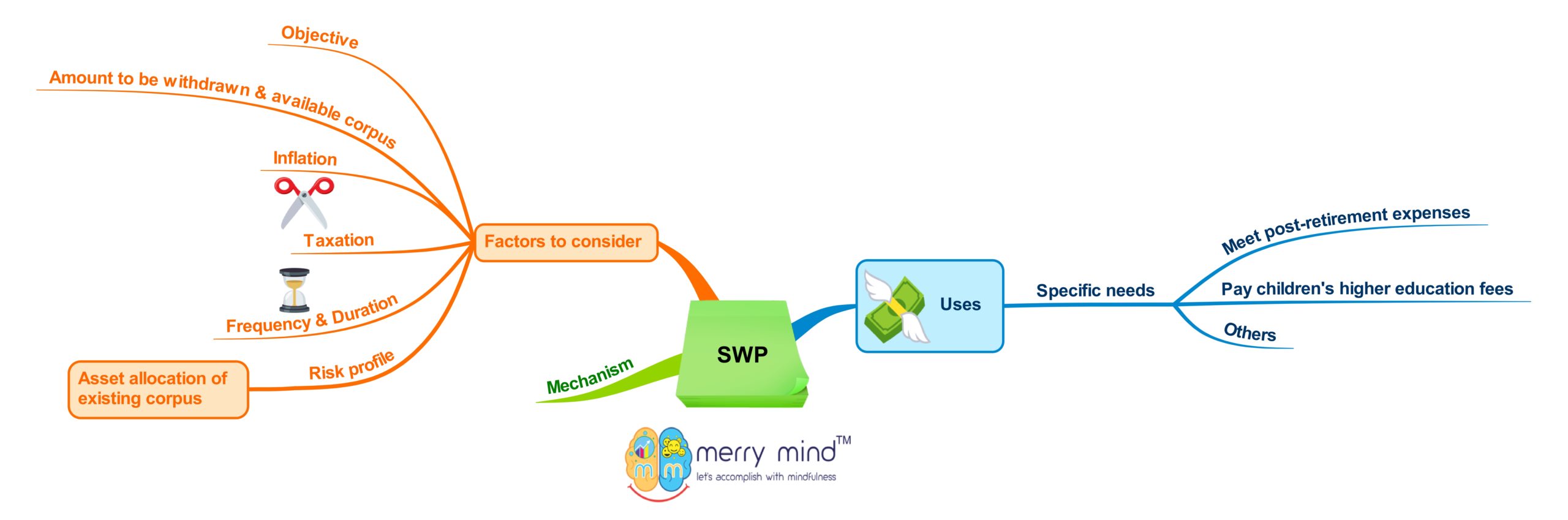

As SEBI Registered Investment Advisor in Kolkata, we initiate Systematic Withdrawal Plan for an investor from his/her existing investments during his/her distribution phase of life i.e. after retiring from work-life. This is a phase where one depends on regular passive income to lead a comfortable retired life. Systematic Withdrawal Plan is a wonderful mechanism which may fulfill your need of passive income at regular intervals.

Again, one may use this mechanism to fund children’s higher education costs. May be fees are to be paid for the next 2 to 5 years. Once the corpus is achieved, instead of withdrawing it all at a time, one may use the SWP route to withdraw money to pay the fees as per requirement (monthly/quarterly/yearly). Here asset allocation will play a huge role to tackle volatility.

How does Systematic Withdrawal Plan work?

Suppose you have Rs. 50 Lakhs with you and you need Rs. 10 Thousand per month as of now. You invest this Rs. 50 Lakhs in Mutual Funds Scheme(s) and withdraw Rs. 10 Thousand per month via Systematic Withdrawal Plan. The scenario may be as follows:

| Month | Investment Amount | SWP Amount | NAV of scheme | No. of units redeemed as SWP | No. of units available after SWP | Investment Value after SWP |

| 1 | 50,00,000 | NA | 100 | NA | 50,000 | NA |

| 2 | 10,000 | 105 | 95.24 | 49,904.76 | 52,40,000 | |

| 3 | 10,000 | 102 | 98.04 | 49,806.72 | 50,80,286 | |

| 4 | 10,000 | 105 | 95.24 | 49,711.48 | 52,19,706 | |

| 5 | 10,000 | 106 | 94.34 | 49,617.14 | 52,59,417 | |

| 6 | 10,000 | 104 | 96.15 | 49,520.99 | 51,50,183 | |

| 7 | 10,000 | 103 | 97.09 | 49,423.90 | 50,90,662 | |

| 8 | 10,000 | 105 | 95.24 | 49,328.67 | 51,79,510 | |

| 9 | 10,000 | 107 | 93.46 | 49,235.21 | 52,68,167 | |

| 10 | 10,000 | 106 | 94.34 | 49,140.87 | 52,08,932 | |

| 11 | 10,000 | 108 | 92.59 | 49,048.28 | 52,97,214 | |

| 12 | 10,000 | 108 | 92.59 | 48,955.68 | 52,87,214 |

How long SWP will last during retirement is a complicated question to address?

Length of SWP depends on the following factors at large:

- Available corpus

- Amount withdrawn

- Frequency of withdrawal

- Financial market scenarios

The corpus you accumulate during your working phase of life, the amount you need to withdraw during distribution phase, i.e. retirement of life and the frequency of withdrawal are unique. Whereas, financial markets are never uniform. When financial markets are doing well, your length of SWP appears to be favourable. Again, when market scenarios are dull or bad, SWP period would be shortened. Your capital may be eroded if appropriate investment plan is not drafted. Role of a qualified Investment Planner is very important to address your needs.

But, will you be in a position to compromise with your monthly needs based on market scenario? Practically, no. This is where asset allocation sets in. As Financial Advisor in Kolkata, we focus in drawing suitable investment withdrawal strategies for our retiree clients.

Challenges in opting for dividend payout option in Mutual Funds

Many investors resort to Mutual Fund schemes with the dividend payout options with the intention to get cash inflows periodically. But, there are quite a few challenges in this approach.

Primary challenge is related to the irregularity both in terms of dividend payouts amount and frequency of such payments. Another shortcoming is tax inefficiency.

Factors to consider while initiating Systematic Withdrawal Plan

You need to figure out the amount you will require as regular income and the frequency of the same. Family cash flow planning is an integral part of financial planning processes. As Certified Financial Planner in Kolkata, we earnestly sit with the client and his/her potential family member(s) to design a cash flow plan. This helps them to understand the corpus they’ll need at retirement. It is evident that with change in scenarios, requirements will change. Financial Plan review at periodical intervals helps us to incorporate the changes within the Financial Plan and stay on track towards financial well-being.

Risk profile is not only the cornerstone to formulate investment strategies during investment period but it has huge relevance during withdrawal phase i.e. when SWP starts. Asset allocation is the key in both the cases – investment period and withdrawal phase to take care of market scenario, taxation and inflation.

Fruitful utilization of SWP mechanism leads you towards a disciplined approach. As Fee Only Financial Advisor in Kolkata, we have been seeing that people are being misguided when it comes to using SWP mechanism. Starting SWP randomly from a scheme without following suitable asset allocation strategy can be counter-productive.