Any choice is difficult because it also means sacrifice. Choosing something inherently means giving up something else. While taking any decision you have to be rational. But, do you know how to behave rationally while taking major decisions in life? During the decision-making process, primarily, you need to consider two aspects. One is technical side and the other is your personal side. Technical side includes mathematical calculations. On the other hand, personal side includes relationships, emotions, hopes, aspirations, self-esteem, sense of well-being, etc. Both sides are equally important and complex. You will agree that, mostly, it is our personal side that drives our decision-making ability. When it comes to deciding whether to buy own residential property or to go on rent, is a dilemma that majority of us may face. There is enormous grey area that exists between the two options. Rent vs Buy is a contentious issue. As Certified Financial Planner in Kolkata, we intend to give uniform importance to both technical and our personal aspects.

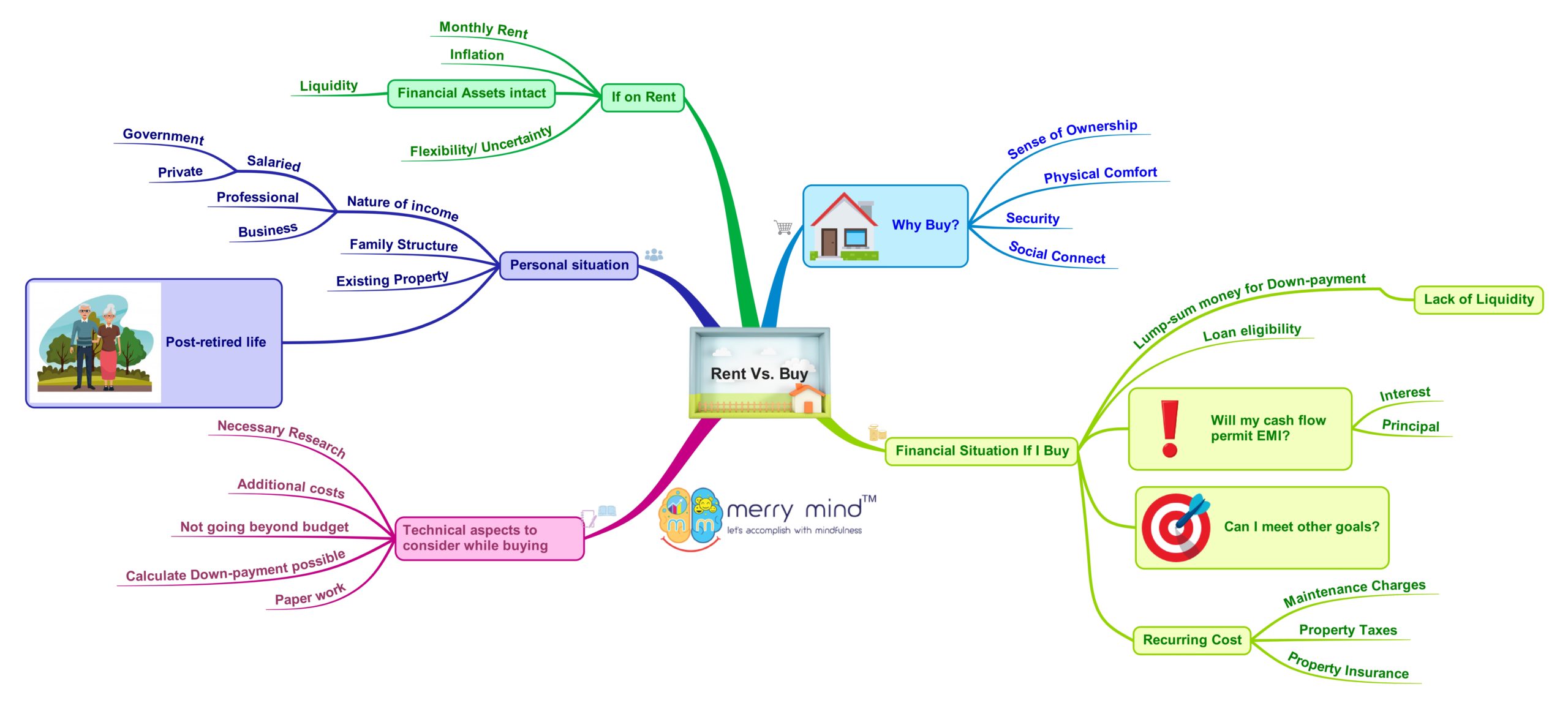

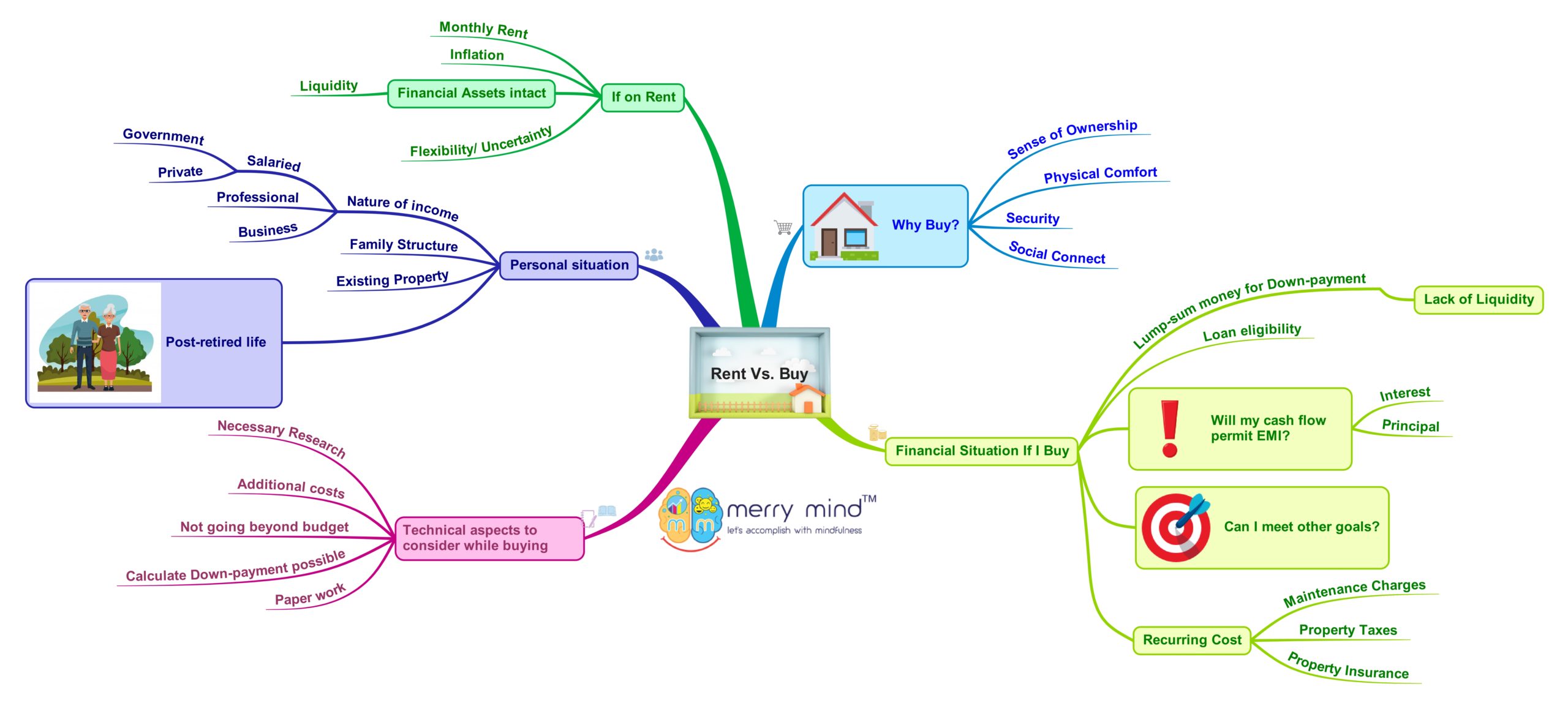

Personal side of buying a residential property

If you start uncovering our desire to buy a residential property, it is evident that it gives a sense of ownership. Many consider owning a residential property as a financial achievement. In addition to that, you get a different level of physical comfort when compared to staying at a rented place. Psychologically, owning a home often imparts a sense of security to homeowners. Social connect is integral to well-being. Social connections develop as you stay in a housing society/complex/locality for a long time. Degree of the same varies.

Your income is a significant frame of reference. Whether you’re a government/ private salaried employee or a professional, it matters as you do Rent vs Buy analysis.

Technical side of buying a residential property

Again, there are a few basic matters to be paid due attention to.

- You need to chalk out your priority criteria.

- Necessary research about builder, locality, etc. must be done before finally taking the decision.

- While making sure to stick to your budget, you need to take into account the additional costs involved. Additional costs may include cost of garage space, interior decoration, etc.

- Paper-work must be clean and clear, etc.

Financial situation if you buy a residential property

You need to understand, calculate and analyze the following relevant questions. This is an exercise during the decision-making process:

- What is the total cost of residential property?

- Am I eligible to take a home loan? If yes, what are my options?

- How much down-payment can I afford to make? What would be the source of the down-payment? I should not disturb my “Contingency Fund”.

- Will my cash flow, after meeting my current expenses and goal-based investments, permit me to pay EMI?

- Can I meet my other financial goals viz. provision for children’s education & marriage, provision for own retirement, etc.?

- Residential property is going to be my fixed and personal asset. Basically, it is an illiquid asset. In case, I make the down-payment and start paying EMIs, I may face liquidity crunch. Do I have enough financial liquidity?

- I will have to bear recurring costs. It includes monthly maintenance charges, property taxes, property insurance premium, etc.

Addressing the above matters may enable you to understand our financial soundness. Thereby, you may be in a better position to decide on the issue of Rent vs Buy.

Technical factors if you go on rent

You’ll have to bear a monthly rent. On account of inflation, your rental expenses are to increase by a certain percentage every year or every two years. On the other hand, your financial assets will be intact. You need not have to pay down-payment. Thereby, you can enjoy financial liquidity.

Evaluate your personal situation if you go on rent

As Financial Advisor in Kolkata, we understand that everyone’s personal situations are always unique. Your present family structure will play one of the vital roles in your decision-making process. You need to consider your career opportunities as well. You may have to move to a different city/ country on account of career opportunity and if your family will accompany you, it demands proper consideration and discussion. Will you return to your home town after your retire from work-life? If so, scenario analysis should be done accordingly. If you have parental property, that will come to the equation too. From one outlook, if you are going on rent, you may have the flexibility of changing places. On the flip side, there’s a bit of uncertainty due to insecurity. Need to frequently change rental accommodation can become hectic for the family. Specially, if elderly parents are staying with you, you may become a challenge.

Mathematical Analysis of Rent vs Buy

Scenario 1: You are buying a residential property

Cash outflow will in the following way:

- One time – Down-payment

- Recurring (monthly) – Home Loan EMI, flat maintenance charges, insurance premium, property taxes, etc.

Assumptions:

- Property cost is Rs. 1 Crore.

- Down-payment is Rs. 20 Lakhs (being 20% of total cost)

- Home loan of Rs. 80 Lakhs is taken for 20 years, where loan interest is 8.5% p.a.

- Property value appreciates 6% p.a.

- Yearly recurring expenses are Rs. 24 Thousand for first 10 years. Thereafter it is inflated by 5% for next 10 years.

Scenario 2: You are going on rented property

Cash outflow will in the following way:

- Recurring (monthly) – Rent

Assumptions:

- Monthly rent for 1st year will be Rs. 3.60 Lakhs

- Rent is expected to increase 5% p.a.

- Investment return is 10% p.a. if you invest your saved money for 20 years.

| Year No. | Rent paid ( A ) |

EMI paid ( B ) |

Other related expenses ( C ) | Difference invested if on rent p.a. [ D = (B+C) – A ] | Years available for investment | Future Value |

| 1 | NA | NA | NA | 20,00,000 | 20 | 1,34,55,000 |

| 1 | 3,60,000 | 8,33,112 | 24,000 | 4,97,112 | 20 | 33,44,321 |

| 2 | 3,78,000 | 8,33,112 | 24,000 | 4,79,112 | 19 | 29,30,205 |

| 3 | 3,96,900 | 8,33,112 | 24,000 | 4,60,212 | 18 | 25,58,741 |

| 4 | 4,16,745 | 8,33,112 | 24,000 | 4,40,367 | 17 | 22,25,822 |

| 5 | 4,37,582 | 8,33,112 | 24,000 | 4,19,530 | 16 | 19,27,728 |

| 6 | 4,59,461 | 8,33,112 | 24,000 | 3,97,651 | 15 | 16,61,085 |

| 7 | 4,82,434 | 8,33,112 | 24,000 | 3,74,678 | 14 | 14,22,837 |

| 8 | 5,06,556 | 8,33,112 | 24,000 | 3,50,556 | 13 | 12,10,214 |

| 9 | 5,31,884 | 8,33,112 | 24,000 | 3,25,228 | 12 | 10,20,705 |

| 10 | 5,58,478 | 8,33,112 | 24,000 | 2,98,634 | 11 | 8,52,037 |

| 11 | 5,86,402 | 8,33,112 | 25,200 | 2,71,910 | 10 | 7,05,264 |

| 12 | 6,15,722 | 8,33,112 | 25,200 | 2,42,590 | 9 | 5,72,014 |

| 13 | 6,46,508 | 8,33,112 | 25,200 | 2,11,804 | 8 | 4,54,020 |

| 14 | 6,78,834 | 8,33,112 | 25,200 | 1,79,478 | 7 | 3,49,752 |

| 15 | 7,12,775 | 8,33,112 | 25,200 | 1,45,537 | 6 | 2,57,827 |

| 16 | 7,48,414 | 8,33,112 | 25,200 | 1,09,898 | 5 | 1,76,992 |

| 17 | 7,85,835 | 8,33,112 | 25,200 | 72,477 | 4 | 1,06,114 |

| 18 | 8,25,127 | 8,33,112 | 25,200 | 33,185 | 3 | 44,170 |

| 19 | 8,66,383 | 8,33,112 | 25,200 | -8,071 | 2 | -9,766 |

| 20 | 9,09,702 | 8,33,112 | 25,200 | -51,390 | 1 | -56,529 |

| Total | 1,19,03,743 | 1,66,62,240 | 4,92,000 | 72,50,497 | – | 3,52,08,554 |

Inference

If you buy residential property, value of property after 20 years may become Rs. 3.21 Crores approximately. Total EMI paid over a period of 20 years will come to Rs. 1.67 Crores approximately. While down-payment at the beginning was Rs. 20 Lakhs.

If you go on rent, you may save money as you are not required to pay Home Loan EMI, flat maintenance charges, insurance premium, property taxes, etc. If you invest your savings per year for 20 years, you may accumulate Rs. 3.52 Crores.

As Financial Consultant in Kolkata, we believe there’s no straight answer to this. Drawing conclusion based on only the technical analysis will not be right.

As SEBI Registered Investment Advisor in Kolkata, we have given a basic mathematical example along with hints relating to personal matters. The choice between renting and owning is a tough one. Sometimes it’s smarter to go on rent and sometimes buying can work in your favour. It’s more helpful to learn the rules, crunch the numbers, consider your personal situation and decide thereafter. Only a careful analysis would help one to reach a proper conclusion.

You may consult a Fee Only Financial Advisor in Kolkata for detailed clarification and unbiased guidance.