Situations in life can change at the drop of a hat. Unforeseen circumstances often put us under pressure. Negative events not only challenge our mental well-being but also our financial situation is put on the line. If cash flow and contingency fund are limited, they can create trauma. A Contingency Plan is a course of action designed to help you to effectively respond to a hasty future event or a damaging situation that may or may not happen.

Contingency planning is a component of risk management, disaster recovery and potentially running your family with minimum jerks. As Certified Financial Planner in Kolkata, we focus in meticulously preparing a comprehensive Contingency Plan which can considerably empower you to come up against abrupt and negative episodes. Thereby, you can retain your financial well-being.

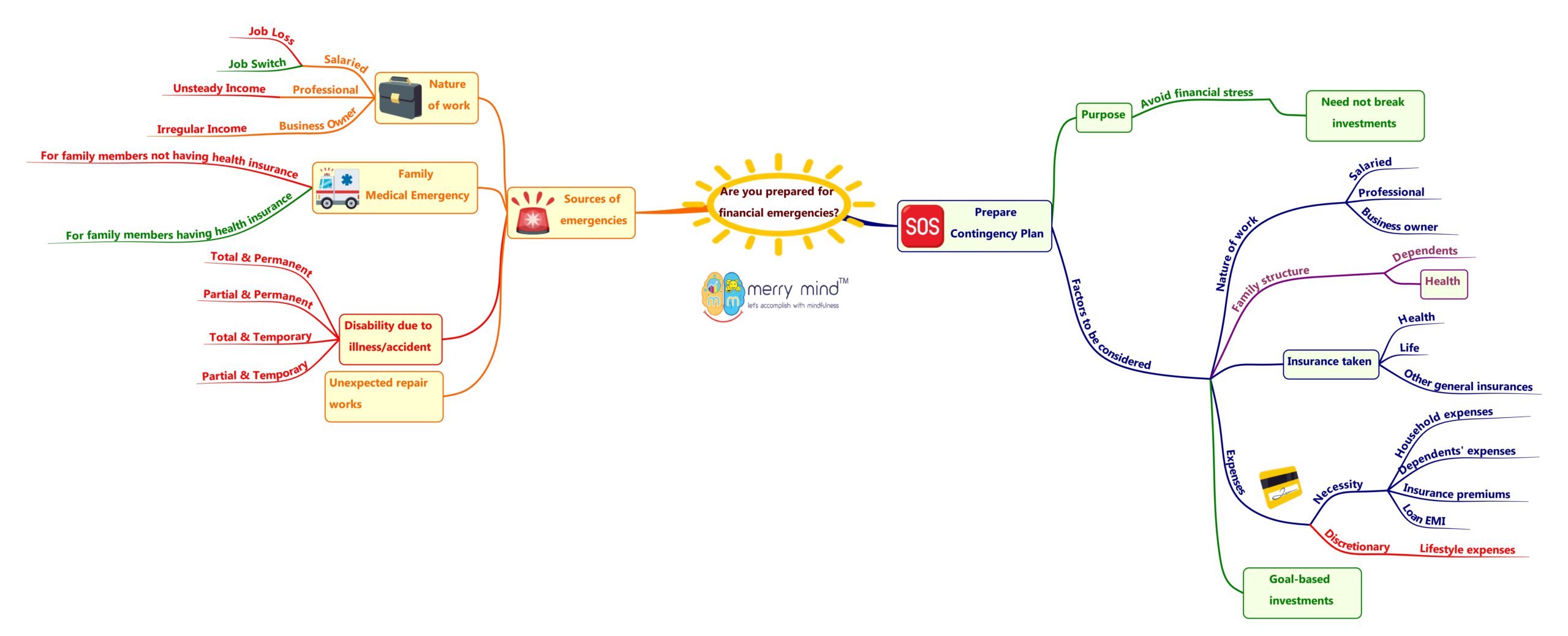

Sources of Emergencies – Need of Contingency Plan

From our experiences in working with our individual and family clients, we have noticed few sources of emergencies which have the capacity to unsettle your family finances.

Nature of work

As Fee Only Financial Advisor in Kolkata, we keep advocating that you need to have Contingency Plan based on your nature of work. If you’re a salaried employee, working in a highly competitive and dynamic industry, you need substantial contingency fund. Due to evolving environment, you may experience lay-off. Covid-19 pandemic has amplified the practicality of being sacked by your organization. Even employees are experiencing salary cuts. It is unfortunate and can happen with anyone. Even, you may decide to switch your job. These will have major financial impacts in your life. In either of the cases, it may take months or even a year before you get a job offer. This is irrespective of your educational qualifications, designation, work experience, etc. When you are jobless, will your family expenses stop? In order to sail through distressing times, your contingency fund will help you to run the kitchen and focus more on your career aspects.

If you a professional, your income may not be steady at all times. There will be periods you’re your practice will bloom. Again, there will be phases of struggle. Businesses go through cycles depending upon the economic and industry factors. As a matter of fact, your Contingency Plan should have provision for periods of fall in earned income. Contingency Plan for business/profession and for family must be kept separately.

Family medical emergency

Medical emergencies may hit any of us any time. To avoid financial stress, people take health insurance cover for the family. The adequacy of your family’s health insurance cover is to be reviewed. Even then, you may have to initially bear the advance payments to hospital. Again, if cashless facility is not available, then you’ll have to pay entire hospital bills and apply for reimbursement later. If you do not make provision for the same in your Contingency Plan, then you will be compelled to liquidate your goal-based investments irrespective of market conditions. Consequentially, you get derailed on your journey of achieving your financial goals.

On the other hand, your parents or other family members may not be medically fit. So, health insurance cover will not be available for them. In case of their hospitalizations, you need to bear the entire cost of treatments. Therefore, it is must to maintain a fund to meet medical expenses of uninsured family members, especially if they have medical history. This will ensure that your goal-based investments are not withdrawn abruptly. This is a major factor in planning for contingencies.

Disability due to illness/accident

Accident results in not just death, but disability too. If any family member, specially the principal breadwinner of the family is disabled due to any illness or accident, it is a dreadful experience for the family. Although hospital bills may be met by health insurance cover, what about medical expenses that will continue later on? Income may cease. Family expenses will practically increase because of additional medical bills. While one may recover from temporary disability, it is not possible to fully recover from permanent disability. Income producing capacity may be lost temporarily. Getting back to normalcy may take months or years. It is miserable to even think of a scenario where the person may never get his/her normal life back. Even then, family expenses will exist.

Tragic events can pull you back mentally as well as financially. As Financial Advisor in Kolkata, we strongly promote application of risk management techniques and proper contingency planning before anything else. The point is to make necessary provisions for the harsh realities of life and get peace of mind.

Your greatest asset is your capacity to earn at present and in the future. It is always advisable to be prepared of the negative consequences in life and make a Contingency Plan for your family. The objective is to ensure that you and your family members are financially equipped to handle unforeseen events.

Unexpected repair works

There are few expenses which crop up without warnings. Car repair works, replacement/ repair of electrical home appliances, home repair works, etc. are a few practical examples which may disturb your regular cash flow if not provisioned for separately.

Factors to be considered while making Contingency Plan

- Nature of work: The work you do influences the level of your contingency fund. The industry/ sector you are in matters. Qualifications and work experiences play important roles too. So, requirement of salaried employee will differ from that of a practicing professional.

- Family structure: To consider the number of dependents in a family i.e. children and elderly parents, their health and other specific needs is a significant aspect in deciding the amount of contingency fund to be earmarked.

- Existing insurance portfolio: Significance of existing insurances (health, personal accident, property, car, etc.) is huge. This gives a fair idea to take further steps relating to risk management and emergency planning. Corrective actions may be required to set things right. The primary objective is financial security.

- Family expenses: Grossly, family expenses may be bifurcated into two sections. One being absolutely necessary expenses and the other is discretionary expenses. Necessary expenses are such that one cannot live without. In times of crisis, you may be in a position to cut down your discretionary expenses. Necessities include household needs, expenses of dependents, EMIs (if any), insurance premiums to keep policies in force, etc. If we consider the Covid-19 pandemic, we can analyze which expenses are necessary for our family’s survival and which expenses can be done away with.

- Ongoing investments: You would certainly not want to compromise with your financial goals by stopping/ liquidating investments. Contingency Fund should contain provision to continue your goal-based investments during unforeseen episodes.

All important question – How many months of contingency fund is sufficient?

The Contingency Plan should be a living document that is updated regularly as per your personal and financial situations. No thumb rules must be followed. Your personal and financial situations are unique. People used to think that contingency fund of 3 to 6 months of family expenses are enough. Covid-19 pandemic is changing people’s mindsets. Now, they feel keeping total family expenses of 8 to 12 months as contingency fund may be fine. Is it so? As Financial Consultant in Kolkata, we strongly believe that the above stated factors must be critically analyzed while formulating a comprehensive Contingency Plan.

You may consult a qualified Personal Finance professional to develop your Financial Plan, where contingency planning is an integral part. Once you have a solid Contingency Plan in place, you can focus on other areas of personal finance with peace of mind.